An intriguing op-ed by Leah Callon-Butler in CoinDesk today obtained me to change my mind regarding something rather essential.

She asked: “Is crypto fintech?”

Yet something regarding that rationale really felt a bit glib, so I wrestled with it some more. And then some much more. As well as after means as well long staring at the screen and wrinkling my forehead, I might be taking tentative enter the “yes” camp, but with some heavy cautions.

What is ‘fintech’?

To start, let’s look closer at what we imply by “fintech.”.

The term is the portmanteau of “financial” and “innovation,” and a lot of meanings stress the latter’s influence on money. “Finance” is usually specified as “the administration of money.”.

Does crypto help with the administration of cash? They may have money-like qualities, cryptocurrencies are not yet normally identified as such * as they are not extensively accepted as a tool of exchange. Yet they can help relocate money around, enable it to express viewpoints in new types as well as create returns in creative ways.

Of all the meanings of fintech from official organizations that I’ve checked out, the Financial Stability Board’s option of words is probably one of the most inclusive: “Technologically enabled monetary technology that can result in new service versions, applications, processes or products with an associated product result on economic markets as well as establishments and the provision of financial solutions.”.

Brand-new service versions. New applications and also processes. Associated product result on economic markets and also organizations.

The “technically made it possible for economic advancement” component is maybe bothersome, as crypto is about a lot greater than “economic innovation,” however it’s not wrong.

What is ‘crypto’?

We should probably define “crypto” as well. The term comes from with cryptography, which relates to the protection of info, as well as is commonly used in its abbreviated form to refer to all things blockchain, including cryptocurrencies, symbols, wise contracts, and so on.

The majority of these principles are being taken on by the financial globe to attempt to re-imagine just how securities move, exactly how firms can increase funds, and also even exactly how currencies operate.

This previous week Standard Chartered, about as “traditional money” as you can obtain (its beginnings go back to 1853), revealed the pending launch of a crypto custodianship service. Even more information are arising on the plans of PayPal, long a darling of the fintech field, to supply crypto services. MUFG, Japan’s biggest banking firm, is creating its own crypto token for usage in a smart device repayment app.

In his prompt record for crypto API supplier Zabo called “Fintech Adoption of Cryptocurrency,” Alex Treece highlights exactly how the turning out of crypto-asset solutions enhanced evaluations of fintech companies Robinhood, Revolut and also Square. Visa provided a declaration this week in which it boasted that it was “improving how money crosses the world,” and in the really next sentence spoke about the “amazing opportunity” of electronic money.

So, fintech seems to be significantly welcoming crypto. Is crypto fintech? It does appear to be becoming part of the fintech collection. It is a modern technology affecting just how money is managed. In some methods it is– but it’s likewise even more than that.

Time for a refresh?

We must keep in mind that the term “fintech” is trying to put an edgy spin on an olden idea. Financial development is not new, as product modifications to how cash is managed were triggered by the telegraph, telephone, central ticker solution, complex by-products and more.

Even in its modern application, it is ending up being outdated, because there are few conventional finance firms that do not currently greatly rely upon new innovations to get to and expand customer bases.

Provided the impact of crypto-based development on our understanding and application of monetary concepts, definitely we can think of something better. Making use of an exhausted catch-all for something so significant resembles attempting to put a powerful push into a tidy bucket.

Much, the innovations making the largest waves in fintech are the web as well as AI– they are game-changing, for certain, but their development stems from the creation as well as therapy of substantially new types of information.

Crypto is additionally a data development, however it goes much even more– it’s a development of authority. And given that the power of finance stems from the authority conferred to it and also by it, the prospective effect of crypto goes beyond what previous modern technologies have handled to achieve.

The modern technologies we put on finance matter, as innovation forms what we do as well as how we do it. The internet, as an example, altered just how we execute old-time tasks such as creating letters or grocery buying. It additionally gave rise to completely brand-new activities such as video clip conferencing and combating zombies (a minimum of I think that’s new).

Fintech has been a transformative pressure; transforming economic practices and also attracting new audiences is no little task. Crypto should be thrilled that it is being considered a tool that can join traditional monetary development. Yet it is not mosting likely to go for simply that.

The impact of new modern technologies on just how we deal with cash should not be taken too lightly. But no technology until now has attempted to change our understanding of cash.

Any individual understand what’s taking place yet?

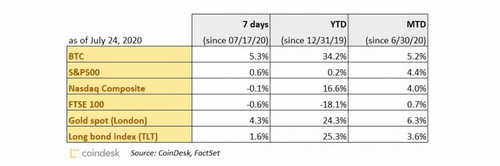

Today in markets had both good information as well as poor.

On the bright side, they say that times of situation bring individuals better together. The European rescue package was seen as a step toward higher fiscal unity, and also has actually increased financier view in European markets as well as in the euro.

And also, sometimes of creating, S&P 500 year-to-date returns are currently in positive territory, which is amazing. Gravy train is clearly an extra powerful market motorist than high joblessness, geopolitical tensions and also unpredictable growth.

The buck, on the other hand, is trending weak versus many significant currencies, as well as looks headed toward its worst month considering that early 2018. The COVID-19 situation tally remains to go from bad to worse, China-U.S. relations have hit a brand-new low and the chance that the global economy may not get better after all appears to finally be sinking in.

Bitcoin appears to lastly be vacating its blues, climbing over the weekend break to get to a gain of practically 10% on the week. Could this be the reawakening of crypto pet spirits?

CHAIN LINKS.

This news is possibly a huge offer: The Office of the Comptroller of the Currency (OCC) stated in a public letter that any type of nationwide bank can now safekeeping digital properties for its clients.

Previously, wardship has actually been the province of specialist companies, which generally required a state permit, such as a count on charter, to provide the service to institutional investors. Now, large, controlled economic companies that already offer comparable safekeeping solutions for stock certifications and the like might broaden their solution.

Lots of institutional financiers are probably more probable to utilize a custodian they are already knowledgeable about as well as who has a line to federal bucks, a better-capitalized annual report as well as insolvency rules that safeguard customer properties.

Caitlin Long points out that there is still lawful uncertainty for financial institutions transacting with crypto properties in the U.S., because commercial legislation treatment of numerous crypto assets is still unclear.

She likewise explains why a bank license absolutely exceeds a count on charter as well as New York’s BitLicense when it involves crypto wardship, which existing custodians are going to have to combine with banks to stay competitive.

Additionally, it is probably more efficient for banks to purchase the technology and know-how than try to build it from the ground up.

It is unclear whether financial institutions will certainly be allowed to extend their custodianship services to cover the quickly growing need for staking, in which digital properties are locked up in particular purses for governance objectives, in exchange for a return.

A substantial part of financial institutions’ custody services for typical properties includes safety and securities loaning– will they likewise go into the crypto lending service?

Alex Mascioli, head of institutional solutions for digital possession prime broker Bequant, advised us that we must not anticipate a charge of traditional banks into the crypto property space– most do not care.

My associates Nik De as well as Ian Allison talked with Washington experts who agree that financial institutions are not likely to move quickly here, and that bigger financial institutions are most likely to desire even more confidence prior to they get in the room.

The OCC is currently directed by Brian Brooks, a previous executive at crypto exchange Coinbase. We anticipated him to attempt to push forward crypto-friendly reform, yet to be truthful I didn’t think he would certainly have the ability to get something this substantial with so promptly. This leaves me confident that there may be much more favorable shocks in store.

Requirement Chartered has actually disclosed that its endeavor and also development arm has been functioning on a crypto guardianship offering for the institutional market as well as the very first pilot can launch later this year. Obviously it was thinking about setting up a crypto market, but understood that a considerable obstacle for its customers was the lack of big-balance-sheet protection solutions.

Avanti, a crypto-focused monetary business referred to as a Special Purpose Depositary Institution (SPDI) based in Wyoming and founded by veteran crypto advocate Caitlin Long, will release in October. TAKEAWAY: Avanti intends to compete with conventional banks for crypto business, and also has a head start, not just in terms of its crypto integrity (Caitlin Long has actually contributed in pushing forward blockchain-friendly legislation in Wyoming, which various other states are starting to replicate). It likewise has the adaptability to introduce on just how financial works, and has begun with a token called the Avit. Details are still slim, however it seems like it will certainly be an electronic token for negotiation purposes, not pegged to the U.S. dollar but issued by a bank under existing U.S. business legislations, which provide transaction finality. I’m expecting discovering more about this.

The price of ether, ethereum’s native token, has actually greater than doubled up until now this year, dwarfing bitcoin’s +34% rise. Yet its fees have actually climbed by far more, signalling growing congestion on the network. ETH charges are now balancing well over $1 per purchase, up from simply $0.04 at the beginning of the year.

TAKEAWAY: Proposals are in the jobs to change the fee framework, and also the entire network is heading towards an extensive technology adjustment that should resolve the scaling problem (we study the upcoming adjustment in detail in our latest record “Ethereum 2.0: How It Works and Why It Matters”). These modifications will require time, nevertheless, and escalating fees tend to eventually choke activity on a network. In the meantime, however, the deal matter is revealing no indicators of easing off. Worth watching.

indeed, we’re also questioning what the charge spikes were for …

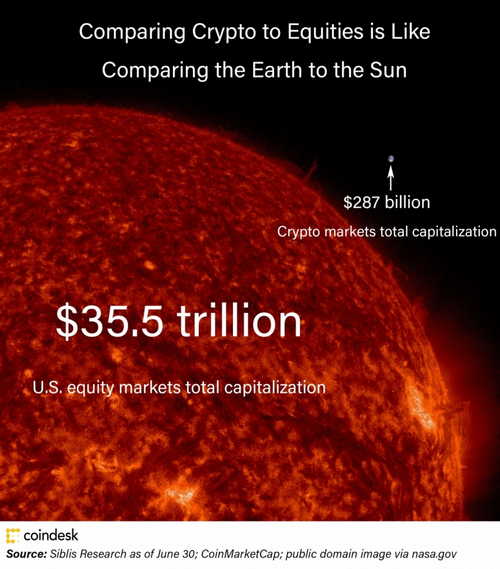

The universe of provided crypto business is still tiny (my coworker Matt Yamamoto has composed records on 2 of them: Ebang and also Hut 8), however that could well change in the extremely near future. TAKEAWAY: With Ant Financial detailing on the Hong Kong and also Shanghai exchanges, and also a reported Coinbase listing in the offing, there can quickly be high-market-cap chances for all kinds of capitalists. A debate can be made that this would be even much better for the field than a bitcoin ETF, as funds moving right into detailed crypto business would certainly spread out conventional investment throughout a range of crypto assets as well as blockchain applications, instead of simply bitcoin.

To obtain a suggestion of the potential influence of even a teensy section of U.S. equity financial investment reaching the crypto market, my associate Shuai Hao prepared this scorching graphic:.

A little global point of view …

And for any current or future token lovers available that have youngsters (or were when one themselves), you can now obtain a Dr. Seuss collectible non-fungible token (NFT) of your really own. TAKEAWAY: NFTs might sound like a quirky niche application currently, however they can end up playing a considerable function in markets with the creation of investment chances in art. Or, and right here it could get even a lot more fascinating, in identification applications. An NFT essentially appreciates all the same advantages of blockchain-based tokens (simplicity of transfer, traceability, sovereign control, etc)– but there is a verifiably restricted number. Maybe one, maybe 10 or 100, yet the scarcity and lack of fungibility become part of the value proposition.

if you assumed CryptoKitties were cute .

Even more details are arising on the strategies of PayPal, long a darling of the fintech industry, to provide crypto solutions. Crypto should be thrilled that it is being thought of as a device that could join traditional financial development. Avanti, a crypto-focused economic firm understood as a Special Purpose Depositary Institution (SPDI) based in Wyoming as well as started by veteran crypto advocate Caitlin Long, will certainly release in October.

TAKEAWAY: Avanti intends to compete with traditional financial institutions for crypto business, as well as has a head begin, not simply in terms of its crypto integrity (Caitlin Long has actually been important in pressing forward blockchain-friendly legislation in Wyoming, which other states are starting to imitate). An argument can be made that this would certainly be also better for the sector than a bitcoin ETF, as funds flowing into listed crypto companies would spread out traditional investment throughout a variety of crypto possessions and blockchain applications, instead than just bitcoin.